Can You Gift Money for a Down Payment? Yes! And Here’s How

These days, it can be pretty tough to scrape together a good chunk of change to use as a down payment for a home. The financial recession, housing crisis, and weak job market hit a lot of Americans hard.

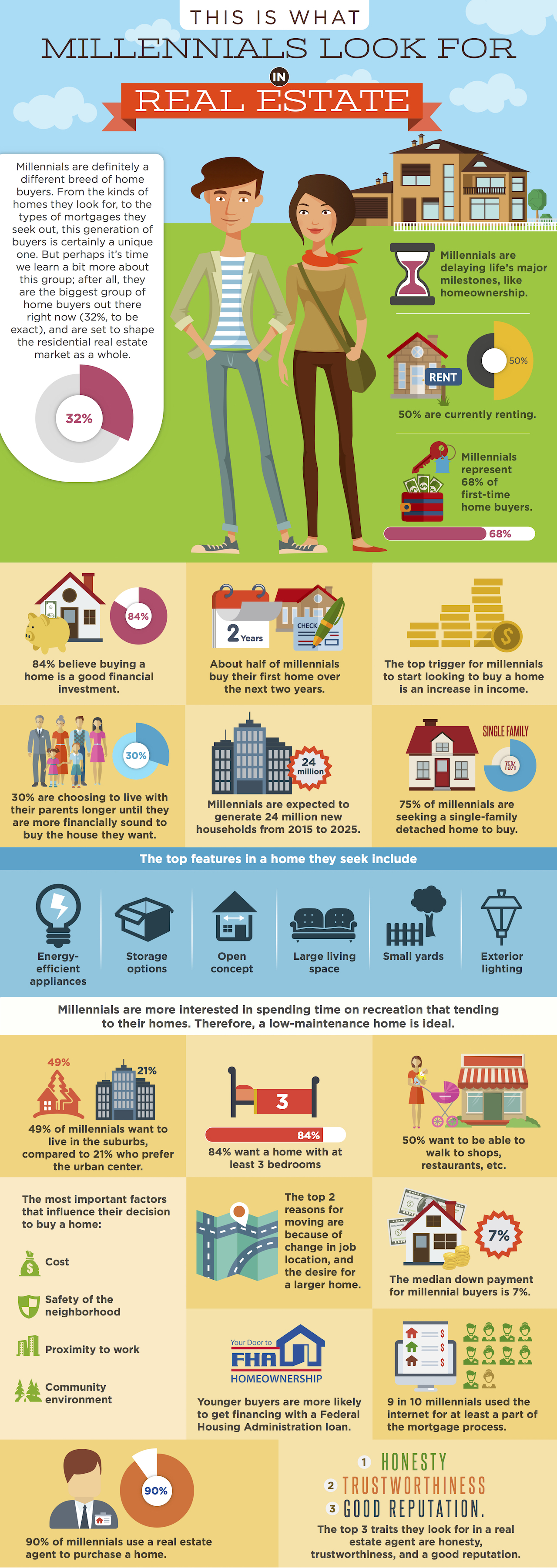

And the millennial generation of today is taking their time moving out of their parents’ homes specifically because they simply cannot come up with enough money to warrant a half-decent down payment.

In fact, more parents are helping out their adult children purchase a home these days compared to decades past; 17 percent, to be exact, according to a recent survey.

Depending on the exact type of property being purchased, its location, the lender, and the type of mortgage, the down payment on its own can be a huge sum. In order to help cover this expense, many buyers turn to family and friends to chip in. And while that’s helpful and all, there are actually certain rules that apply to this type of gifting before the funds can be used to put towards a home purchase.

The Money’s Got to Come From Family

While you might be generous enough to want to financially help out your co-worker’s niece or your best friend’s son to buy a home, your money won’t be good in these circumstances. You can gift down payment funds to your kids, grandkids, and even your siblings, but not to your neighbor, friend, or fourth cousin on your mother’s side.

Not only does it matter who is giving the money, it’s also necessary for the cash to be easily tracked. Lenders want to have total transparency when it comes to where the funds are coming from, and are cautious when it comes to all-cash gifts that are put towards a mortgage. If you’re going to give money as a gift for a down payment, do it through a wire transfer or check instead of cold-hard cash.

Avoiding ‘Gift Taxes’

Seems that Uncle Sam is always lurking when it comes to money, and that’s no exception in the case of gifted funds for down payments. In order to avoid paying taxes on your monetary gift, you need to stick to a cap of $14,000 per individual. However, you and your spouse could give up to $28,000 to one child, which implies two separate gifts. That number can be doubled if you and your spouse are gifting your child if he or she is married. Just make sure that each check is no more than $14,000 a-piece, or you’ll be dinged by the IRS.

Down Payment Borrower Contribution

The rules when it comes to borrower contribution as opposed to a gift will vary depending on the exact type of mortgage. For an average conventional mortgage, all of a 20 percent-or-more down payment can be in the form of a gift. If less than 20 percent is being put down, part of it needs to come from the individual receiving your monetary gift; this amount will vary by loan type.

Fannie Mae requires a 3 to 5 percent contribution from the borrower, and Freddie Mac requires a 5 percent minimum borrower contribution if the down payment is under 20 percent.

In addition, the transaction needs to involve a two- to four-unit property that’s either a primary or secondary home. VA and FHA mortgages will only allow monetary gifts to be used towards primary homes.

Down Payment Gifts Need to Be Well-Documented

The money that you give as a down payment contribution needs to be documented. Usually, mortgage lenders will provide a letter for both you and the individual you’re gifting to sign, which shows that the money was actually a gift and not a loan that will need to be paid back.

Lenders will typically ask for bank statements from those who are planning to use a monetary gift towards their purchase in order to comply with the Patriot Act. They want to know that the funds aren’t going to be used for any nefarious reasons, like money laundering or funding for any terrorist activity.

The rules will vary from one lender to the next, so you’d be well-advised to find out exactly what your beneficiary’s specific lender requires from the both of you.

The Bottom Line

The gift-giving season may have just passed, but the spirit of generosity doesn’t have to. If your loved one is having a tough time coming up with the necessary funds to put towards a down payment, helping them out is a noble gesture. Just make sure you’re aware of the rules that come along with offering gift money for a down payment to avoid headaches and pesky tax implications.

First-time homebuyers might have their own unique set of challenges, but one thing they do’t have to worry about is dealing with the sale of a current home while looking to throw the mortgage onto another.

First-time homebuyers might have their own unique set of challenges, but one thing they do’t have to worry about is dealing with the sale of a current home while looking to throw the mortgage onto another.

2. Rent Prices Are Forecasted to Spike

2. Rent Prices Are Forecasted to Spike 4. Prices of Homes Will Be Scaling Back

4. Prices of Homes Will Be Scaling Back