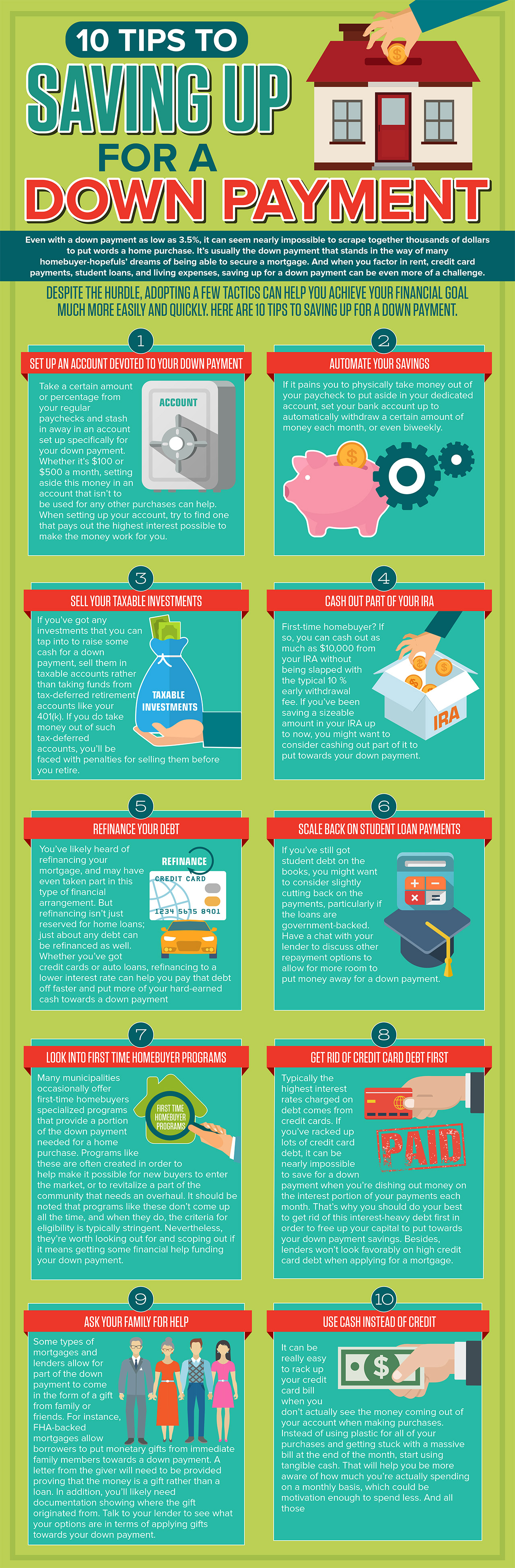

9 Kitchen Design Mistakes to Avoid

No matter how amazing and comfortable the rest of your home may be, there’s something about the kitchen that has everyone congregating to it. No doubt, your kitchen is the hardest working space your home, and should be designed to help make it as efficient as possible. And considering how much of an effect the kitchen has on the overall value of your property, you’d be well advised to make sure its design and style are carefully considered.

After flipping through countless home interior magazines and navigating through Houzz and Pinterest, you’ve probably got a solid idea of what you want your new kitchen to look like. But before you start the process, you’ve got to have a detailed plan in place, which includes things that need to be done, as well as things that you absolutely must avoid.

Here are a few kitchen design mistakes to steer clear of.

1. Not Planning For Adequate Storage Space

Unless you plan on leaving all your pots, pans, dishes and glassware on the counter (which you shouldn’t), you’re going to need to seriously think about adding enough storage to keep all of your kitchen belongings out of sight. And don’t forget about your dry foods and knickknacks that will also need to have a home. Whether your storage takes the form of extras drawers, pantries, or cabinets, you need to be certain that it is adequate enough to tuck everything neatly without having to cram everything into a tight space.

2. Not Including Enough Counter Space

The amount of space that you’ve got on your countertops is equally as important as your storage space. After all, it’s where you’ll be prepping your meals and housing small appliances like your blender, toaster, and coffee machine. And don’ forget about any decorative elements that you may want to have out on your counter to boost the style factor of the room. Without adequate space on your countertops, you’ll find your kitchen will become cluttered really quickly and easily.

3. Skimping on Lighting

If you want to clearly see what you’re doing as you’re preparing dinner, you’re going to need excellent lighting in the kitchen. But many homeowners skimp on lighting in this space for some reason, and often leave it to one solitary central light fixture to provide the lighting needed. Instead, the lighting in your kitchen should be varied, and include both task lighting and fixtures meant specifically for creating ambience.

Consider illuminating the overall space with pot lights, and install pendant lights over your kitchen island. You may also want to install undercabinet lighting to illuminate your counter as you handle food, and hang a chandelier over the dinner table. Layering your lighting in this fashion can provide with both the right amount of lighting needed to whip up your famous dish, while giving you the flexibility to create a specific atmosphere in the space.

4. Lacking Proper Ventilation

All those fumes from your boiled eggs or grilled salmon have to go somewhere, or else you’ll be left with unpleasant smells that will linger for hours. Not only that, but if you have a gas stove, these fumes can go from unpleasant to downright dangerous. That’s where proper ventilation comes into play, which is a critical component to consider in the planning stages of a kitchen design. Not only will an adequate ventilation system help keep the air in your kitchen fresh, it’ll also help to lengthen the lifespan of your appliances.

5. Forgetting About the ‘Kitchen Triangle’

It would be pretty awkward and annoying to have to dodge obstacles to bring food items from your fridge to your stovetop. That’s why the kitchen triangle should always be kept in check during a kitchen design. This layout basically links the three most used areas of the kitchen: the stove, fridge, and sink.

Out of all these components, the sink, in particular, is most often used, and should have direct access to both the fridge and stove. Tight walkways, cabinet doors that swing open the wrong way, and improperly situated islands can mess this system up big time. Straying from the kitchen triangle too much can make the room must less efficient.

6. Misjudging the Island

Having an island in the kitchen can offer you additional counter space and an added spot to eat and hang out. But your kitchen’s size and layout will dictate the size and location of an island, as well as whether or not one can even effectively exist. The kitchen is a working space, so anything that gets in the way of functional flow will just cause problems.

If the island is too big, or is not located in an ideal spot, you’ll cut off proper flow in and around the space. Ideally, there should be between 42 and 48 inches of open area surrounding kitchen islands. For it to be of any use, the island should be at least three by five feet in dimension, and your kitchen should be a minimum of 13 feet wide.

7. Going Too Trendy

Unless you’re planning on revamping your kitchen every few years, you’d be better off sticking to a design that’s not overly trendy. While you still want to be modern and innovative, you also don’t want to be so quirky that the appeal of your kitchen will wear off you in the near future.

Rose Quartz and Serenity might be Pantone’s choice of colors of the year, but how long these pastel hues stay on trend in the next few years is up for debate. No one says you can’t be bold in your color choices, but just be sure to use them in non-permanent ways, such as with your towels or decorative accessories.

And when it comes to kitchen design, carefully consider the styles you choose for your trim, cabinet materials, finishes, countertops, and flooring. You might think you’re certain that the latest out-there trends will tickle your fancy for the long-term, but you never know when your tastes will change, or if you ever plan on selling your home in the near future to buyers that may not necessarily have the same tastes.

8. Forgetting About the Trash

Your kitchen design can be sleek and impressive, but the look of this space can easily be thrown off with the presence of a trash can. Nothing is more off-putting than the sight of garbage, so be sure that you consider a spot where you garbage bin can be tucked away in a spot that’s easy to access.

Not only is the spot for a trash can up for consideration, so is a bin for your recyclables. One modern way that interior designers and homeowners are tackling this issue is by installing a dual cabinet pull-out that features one bin for the trash, and another for the recyclables. This offers easier access, rather than having to reach under the cabinet and hoping that your toss made the bin.

9. Not Including Enough Electrical Outlets

Think about all the little appliances that you’ll be using in the kitchen at various stations. From your toaster, to the cake mixer, to the blender, all these items need an outlet to be plugged into. And what about your smartphone and tablet? Odds are the kitchen counter will be the place to recharge these gadgets. For that reason, make sure you’ve installed enough outlets to accommodate all the things that will need to be plugged in.

Spending the time considering all these factors in the planning stages can help save you plenty of hassles after the fact. Make sure you’ve considered all the components that go into making a kitchen great, and avoid all these mistakes that can wreak havoc on your kitchen design.